• World: Global premium pool expanded by +7.1% in 2025 – an increase of EUR456bn

• Romania: Strong growth of +10.6% – P&C and life drive expansion

• Outlook: Private protection remains a structurally growing need ensuring solid global growth of +5.3% per year over the next ten years

Allianz Research today published its latest “Global Insurance Report”, which analyzes developments in insurance markets worldwide.

World: Cooling from exceptional growth, but far from slowing into weakness

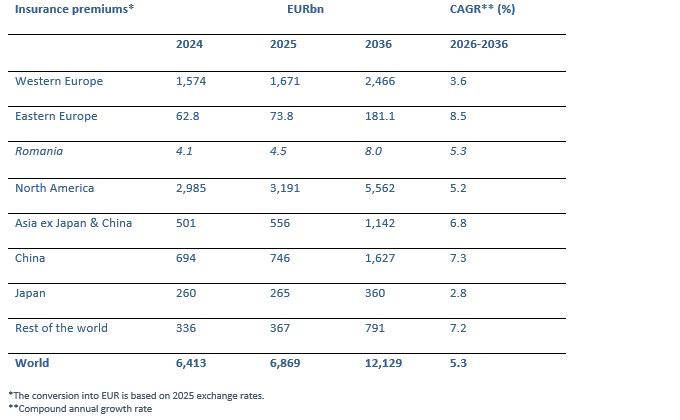

According to the report, the global insurance industry is estimated to have grown by +7.1% to EUR6.9trn in 2025, adding EUR456bn to the global premium pool. Although growth moderated from the exceptional +9.4% recorded in 2024, it remained comfortably above the ten year compound average growth rate (CAGR) of +5.6%, confirming that the industry’s growth drivers remain firmly intact. Life insurance remained the largest segment (EUR2,861bn), followed by P&C (EUR2,320bn) and health (EUR1,688bn).

The P&C market is moving from pricing boom towards normalization. Global premiums increased by +3.8% in 2025, well below both last year’s +8.5% expansion and the segment’s ten year CAGR of +5.6%, as pricing cycles matured and claims inflation began to stabilize. North America remained the industry’s dominant market, accounting for 52% of global P&C premiums, although growth slowed sharply to +2.2% from +9.7% in the previous year. Western Europe remained comparatively resilient with growth of +5.3%, while the Asian1 market was less dynamic expanding by only +4.0%.

The life insurance market remained robust in 2025, although the exceptional post-rate-hike boom in North America has clearly lost momentum. Global life premiums grew by +6.9% in 2025, down from the exceptionally strong +11.3% recorded in 2024 but still comfortably above historical norms. The moderation was driven primarily by North America, where the annuity boom fueled by households locking in higher interest rates has started to lose momentum. Asia has meanwhile re-emerged as the industry’s principal growth engine, with life premiums rising by +9.9% in 2025 and China alone expanding by +11.4%. Asia remains the world’s largest life insurance market, supported by demographic ageing, high savings rates, and less comprehensive public pension systems.

Health insurance is becoming the industry’s clearest structural growth story. Global health premiums increased by +12.3% in 2025, the strongest expansion since 2014, as ageing populations, rising medical costs, and pressure on public healthcare systems continued to drive demand for private protection. North America alone grew by +14.9% as medical inflation accelerated further, with the US now accounting for more than 70% of global health premiums. Despite some normalization following the post-Covid surge, long-term growth potential remains particularly strong in Asia, where health insurance penetration is still below 1% in almost all markets.

Geopolitics and fragmentation are becoming central forces shaping the insurance industry. A more fragmented global economy is making risk environments more complex, challenging cross-border business models and weakening traditional diversification benefits. At the same time, fragmentation is also creating new growth opportunities by increasing demand for protection, resilience and specialized risk transfer across areas such as infrastructure, energy security and political risk insurance. Insurers will need to adapt by building more regionally resilient operating models, integrating geopolitical analysis more directly into underwriting and capital allocation, and developing products tailored to emerging risks.

Romania: Life rebound and P&C strength support double-digit growth

The Romanian insurance market achieved strong growth of +10.6%, with total premium income of EUR5bn. P&C insurance expanded by +8.8%, while life insurance grew by +19.1%, significantly above the 2015-2025 average of -11.1%. Finally, health insurance premiums rose by a strong +10.5%.

Outlook: Insurance remains a growth industry

Overall, the global insurance market is expected to grow at an annual rate of +5.3% over the next ten years, slightly above economic output. For Romania, overall annual growth is expected to be +5.3% (nominal GDP: +5.1%). For P&C, we expect global annual growth of +4.7% up to 2036 (Romania: +3.2 %). The segment will show solid growth rates in almost all markets, as the increasing need for protection is a global phenomenon. Allianz Research also remains confident about life insurance, which can expect annual growth of +4.9% thanks to higher interest rates (Romania: +3.3%). Wider Asia remains the growth engine, driven by the need for private provision in the face of accelerating demographic change. The smallest segment, health insurance, should remain the most dynamic, with annual growth of +6.7% (Romania: +21.6%). Asia in particular still has a lot of catching up to do.

In absolute terms, the global premium pool will grow by EUR5,260bn over the next ten years. Most of this growth will come from life insurance (EUR1,991bn). More than half of this additional premium pool will be generated in Wider Asia (EUR1,004bn), exceeding North America (EUR416bn) and Western Europe (EUR402bn) combined. In P&C insurance, 44% of the additional premiums of EUR1,505bn will come from North America. In health insurance, we expect additional premiums of EUR1,764bn, most of which will come from the US market.

The global insurance map will continue shifting eastward, albeit gradually. North America is expected to retain a global market share of roughly 46% through 2036, surrendering only marginal ground over the next decade (-0.5pp). India and China, by contrast, are expected to continue gaining relevance, together adding almost 4pp of global market share. Western Europe will continue to lose relative weight. A glimmer of hope for the Old Continent: while it lost 5.3pps of market share in the last decade, it may lose "only" 4pps in the next decade.

“Geopolitical fragmentation is reversing many of the assumptions that shaped the global economy for decades,” said Ludovic Subran, Chief Economist and Chief Investment Officer at Allianz. “As trade, capital flows and regulation become increasingly fragmented, resilience is replacing efficiency as the dominant organizing principle. This shift is making the operating environment more complex and costly, making the push for affordability even more urgent. Nothing less than insurance’s strategic importance is at stake: not only as a mechanism for risk transfer, but also as a critical enabler of investment, innovation and economic confidence.”

You can find an interactive “Allianz Global Insurance Map” at our homepage:

https://www.allianz.com/en/economic_research/research_data/global-insurance-map/

You can find the study here on our homepage: Economic Research | Allianz

About Allianz

The Allianz Group is one of the world’s leading insurers and asset managers, active in almost 70 countries and serving around 97 million private and corporate customers*. Our customers benefit from a broad range of personal and corporate insurance services, including property, life and health insurance, as well as assistance services, credit and global business insurance. Recognized for the seventh consecutive year as the number one global insurance brand in Interbrand’s Best Global Brands 2025 ranking, Allianz’s success is built on technology-enabled customer centricity – providing peace of mind, protection, and prevention for our customers and strengthening the resilience of individuals, communities, and societies. We are one of the world’s largest investors, managing around 770 billion euros** on behalf of our insurance customers. Furthermore, our asset managers PIMCO and Allianz Global Investors manage about 2.0 trillion euros** of third-party assets. Thanks to our systematic integration of environmental and social criteria in our business processes and investment decisions, Allianz received an MSCI ESG Rating of AAA (as of March 2026). In 2025, our 156,000 dedicated employees achieved a total business volume of 186.9 billion euros and an operating profit of 17.4 billion euros for our shareholders.

1 Asia always refers to the region excluding China and Japan. If both countries are included, we use the term wider Asia

* As of December 31, 2025. Customer count reflects Allianz customers in consolidated entities that are part of the customer reporting scope only

** As of March 31, 2026