• 11th Allianz Motor Day: Allianz welcomes the EU Data Act – but sees further need for regulation on secure exchange of vehicle data

• Vehicle owners should have full control and sovereignty: they decide who can use the data from their vehicle for specific purposes

• Allianz calls for a regulated marketplace for data exchange and for vehicle manufacturers to demand fair prices for providing data

• The new regulation can strengthen the European digital economy and make our transport systems more sustainable, safer and more effective

• Allianz sees major customer benefits: the EU Data Act enables even more individualized and risk-based insurance premiums, improved accident prevention and smarter claims management in car insurance

• An Allianz survey conducted in five European countries shows that a growing number of car drivers are willing to share their car data with their insurer

A new EU law aims to make data from connected vehicles usable – for the benefit of vehicle owners, to improve road safety and to enable sustainable digital innovation.

The EU Data Act was the main topic at the 11th Allianz Motor Day on October 17, 2023. Experts discussed the new regulation at the Allianz Center for Technology (AZT) in Ismaning.

Vehicle data, used wisely, makes the transport system safer, cleaner, smarter

Allianz’s assessment was clear: “We welcome the EU Data Act,” said Klaus-Peter Rohler, Member of the Board of Management of Allianz SE. “The new law stands for innovation and competition – it is a European initiative to strengthen the European digital economy. The new EU regulation follows a convincing principle: ‘My device, my data’ – we support this idea.” Users of a connected car, according to the new legislation, will in future be able to demand from the manufacturer that the data collected in the vehicle be transferred to third parties. For “easily accessible data,” the EU Data Act even requires the data to be made available in real time.

This, Rohler said, could lead to real innovations: “We want to convince our customers in car insurance, through attractive offers, to share their data with us. The EU Data Act would also give other companies and start-ups the chance to become inventive. Using millions of live camera and position data from vehicles could solve the parking-space problem in inner cities. This would not only be a win for drivers, it would also save significant amounts of energy, help climate protection and improve air quality. If vehicle data is used wisely, it has the potential to make our transportation system safer, cleaner and smarter overall.”

How the EU Data Act could change car insurance

With detailed data from the vehicle, completely new insurance offers can be provided and new services made available in the future. “In case of an accident, it would be possible to automatically record the extent of the damage in real time by evaluating position data and data from crash sensors. Allianz could immediately inform a towing service, reserve a rental car, order suitable spare parts and make a workshop appointment for our customer. In the case of serious accidents, medical assistance could be provided,” Rohler said.

“In the past, the customer had to inform us. In the future, we’d contact our customers proactively, providing relief when customers need us most.”

Rohler also pointed out that by using car data, Allianz can offer the fairest possible price to every customer. “We can calculate insurance offers that are significantly more risk-adjusted, taking into account both the driving style and whether the vehicle is equipped with safety systems and whether those are switched on or off. At the same time, the sensor and camera data can be used for the proper, correct and fair investigation of an accident and for liability clarification,” Rohler said.

Data sent directly from the vehicle will take on special significance when autonomous and AI-supported systems control the vehicle in the future. “Those affected – as well as society – have a right to know whether the human or the machine caused the accident,” Rohler said.

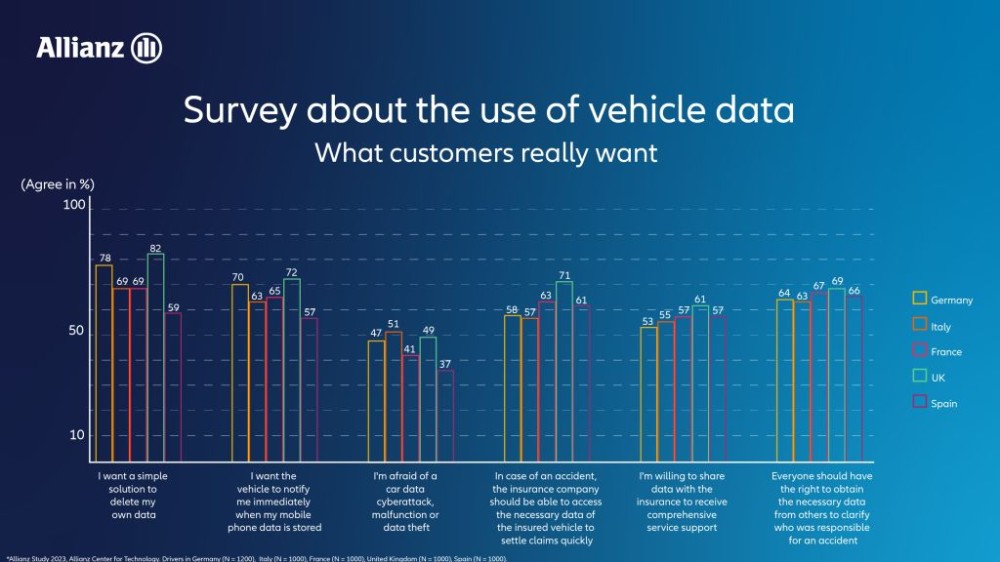

A recent Allianz survey conducted in five European countries shows that a majority of car drivers are willing to share their car data with their insurer if they receive comprehensive service support in return: in Germany it’s 53 percent, in Great Britain even 61 percent. “This is a very important message for us, which we can be proud of: our customers know that they can trust us, because we will handle their data with care and in their own best interest,” Rohler said, commenting on the survey results.

True competition can exist only with fair prices

Discussions at the 11th Allianz Motor Day also revolved around the question of how third parties can access in-car data in practice. The EU Data Act stipulates that “easily accessible data” must be transmitted in real time – but what data is that? And what price may the car manufacturer charge for transmitting the data to third parties? “Real competition can only emerge if vehicle manufacturers demand fair prices. Otherwise, third parties have no chance to innovate,” Rohler said.

Legal framework for data transfer is missing

But what should an individual customer do with the data of their vehicle? And above all, how should they access the data and pass it on? This can only work if there is a very simple way for the individual to transfer the data in practice. “The EU Data Protection Act only creates the legal basis for the transfer of data from the vehicle to third parties. However, the legal framework is still missing that specifies in which technical way the data from the vehicle can be made usable for all market participants,” Rohler said. “Legislators must find a practicable solution for this as quickly as possible, otherwise the treasure trove of data cannot be mined for the benefit of customers and of all participants.”

Regarding the use of vehicle data, Allianz demands the following:

- Vehicle owners must be given full transparency about the data collected in their vehicle. Every car owner must be given a precise overview so that they know what data is being collected in their vehicle. In addition, it must be possible to see which of these data points can be transmitted to third parties in real time.

- In order for car owners to be able to make good use of the newly acquired sovereignty over their vehicle data, a standardized minimum data set is needed to enable new services regardless of the car manufacturer and to allow data to be shared quickly and easily in real time via defined interfaces if the owner so desires.

- Allianz calls for a regulated marketplace and an independent data trustee who ensures the secure exchange of vehicle data. This independent institution must ensure that authorized parties can access data.

- So that drivers can benefit from the many conceivable innovations, we need fair prices for data transmission to third parties. The costs must be calculable to enable broad competition.

All press materials and the recording of the entire event, as well as information on the EU Data Act, can be found here: https://events.techcast.cloud/en/allianz/11th-allianz-motor-day-2023-en

About Allianz

The Allianz Group is one of the world's leading insurers and asset managers with more than 122 million* private and corporate customers in more than 70 countries. Allianz customers benefit from a broad range of personal and corporate insurance services, ranging from property, life and health insurance to assistance services to credit insurance and global business insurance. Allianz is one of the world’s largest investors, managing around 714 billion euros** on behalf of its insurance customers. Furthermore, our asset managers PIMCO and Allianz Global Investors manage about 1.7 trillion euros** of third-party assets. Thanks to our systematic integration of ecological and social criteria in our business processes and investment decisions, we are among the leaders in the insurance industry in the Dow Jones Sustainability Index. In 2022, over 159,000 employees achieved total revenues of 152.7 billion euros and an operating profit of 14.2 billion euros for the group***.

* Including non-consolidated entities with Allianz customers.

**As of June 30, 2023.

*** As reported – not adjusted to reflect the application of IFRS 9 and IFRS 17.