Besides Romania, the analysis covers eight other countries in the region, namely Hungary, Poland, Czech Republic, Slovakia, Bulgaria, Croatia, Serbia and Latvia.

“Granting company shares is a remuneration method based on which the employer connects the individual performance of top management employees with the business performance, generating increased loyalty and, at the same time, additional motivation. Even though the tax regime for such an instrument is definitely more favorable than usual salary elements, when deciding on whether the company should implement such an instrument, the employer should focus on the company’s growth strategy and the need to co-engage the employees in achieving it,” mentioned Raluca Bontas, Partner Global Employer Services, Deloitte Romania.

The tax incentives are the main benefits for the equity plans (more specifically, of the Stock Option Plan), since the taxation occurs when the employee sells the shares and thus obtains a capital gain, and not when he actually receives them, like in the case of other types of benefits.

“The Stock Option Plan has two important elements: the correlation between the remuneration received and the increase of the employer’s shares value and, subsequently, the employee’s retention for a longer period, either to benefit from a higher value of the shares or to obtain the associated dividends,” states Elena Raileanu, Manager, Global Employer Services, Deloitte Romania.

The main conclusions for the equity plans in the nine countries subject to the analysis:

- The applicable laws in Romania, Poland, Serbia, Latvia and Hungary provide similar tax incentives, for certain equity plans, the main difference being that the legislation in Romania is more favorable from a tax perspective;

- in Poland, Latvia, Serbia and Hungary, the tax incentive is the same with the one applicable in Romania, in the sense that the taxation is deferred until the sale of shares;

- however, the income tax for the capital gain is higher: in Latvia 20%, in Poland 19%, and in Serbia and Hungary, 15%, compared to 10% currently in Romania;

- Applicable laws in the Czech Republic, Slovakia, Bulgaria and Croatia do not provide a favorable tax treatment for equity incentives;

- With respect to the equity plans that have a favorable tax treatment, in some of the countries the qualifying conditions are similar to the ones applicable in Romania (for example, in Latvia, the plan has to be a Stock Option Plan), while in other countries, additional criteria apply (for example, in Serbia, the employment period has to exceed two years).

It is worth mentioning that, in addition to the income tax paid for the benefits associated with the enrollment in the equity plans, employees and employers should also take into account the mandatory social security contributions due in each country, based on the domestic and European legislation on social security matters.

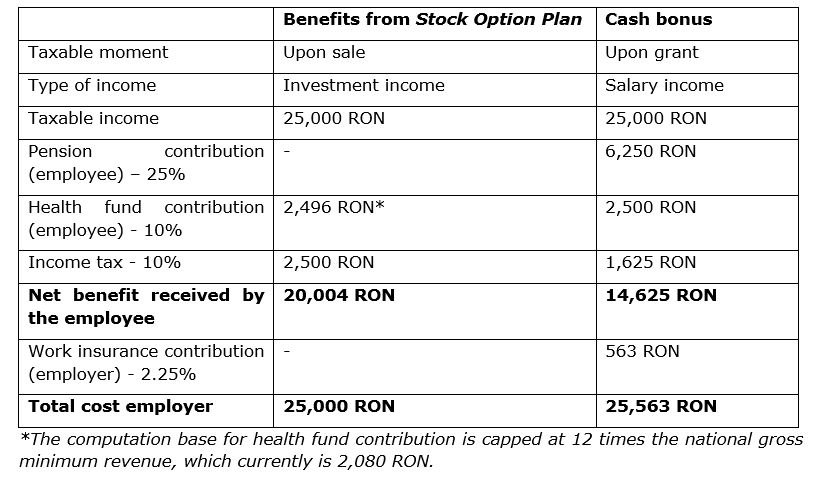

Example

A comparative calculation of the taxation regime applied for benefits received as shares and as cash amounts reflects the advantages generated by the tax incentives in Romania. The estimate computation is prepared based on the assumption that the capital gain obtained from the sale of shares is equal to the cash bonus, so that the outcome is relevant.